![[HERO] Does Your Credit Score Really Matter in 2026? Why Unsecured Working Capital Loans Are Shifting to Cash Flow.](https://cdn.marblism.com/2eztkKx3aeH.webp)

NEWS FLASH: The FICO-first era is sunsetting. As we move through the first quarter of 2026, the traditional credit score, that three-digit number that has kept many a business owner awake at 2 AM, is no longer the end-all, be-all of business financing. The focus has shifted. The pulse of your business isn't found in a dusty credit report from three years ago; it’s found in your daily cash flow.

If you’ve been hesitant to apply for funding because your personal credit score isn't "perfect," it’s time to take a deep breath. At Simplified Capital, we’ve been facilitating programs for business owners since 2002. For 23 years, we’ve watched the landscape evolve, and 2026 is officially the year of the "Cash Flow Comeback."

But does your credit score still matter at all? Let’s dive into the current state of unsecured working capital and why your bank statements might be more powerful than your social security number.

Is Your Credit Score a Relic of the Past?

Let’s be real: your credit score is essentially a snapshot of how you handled money in the past. While it’s still an important metric for mortgages and personal car loans, the modern lending environment of 2026 has realized that a personal credit mishap in 2022 doesn't necessarily mean your business isn't thriving today.

- The Transition to Broader Evaluation. Traditional models are expanding. Today, lenders are looking at "alternative data", rent payments, utility bills, and even Buy Now, Pay Later (BNPL) consistency.

- Payment History Still Matters. While the score itself is less of a gatekeeper, your habit of paying on time remains a top factor. It accounts for about 35% of the old-school calculation.

- The "Snapshot" Problem. A credit score is a moment in time. Cash flow is a movie. Lenders in 2026 want to see the whole film, not just a blurry still frame from a bad weekend three years ago.

Why Cash Flow is the New King of Underwriting

In 2026, unsecured working capital loans are increasingly "cash-flow-based." What does that mean for you? It means that if your business is generating consistent revenue, you are a prime candidate for funding, regardless of whether you hit a bump in the road with a personal credit card back in the day.

When we look at facilitating programs for our clients, we’re looking at the health of the business. Are you doing $20,000, $50,000, or $500,000 in monthly sales? Is that money staying in the account, or is it gone the second it hits?

The Shift Toward Real-Time Data:

Lenders now use secure API connections to view your business bank activity. This allows for a "Soft Pull" (which you can learn more about at https://www.simplifiedcapital.com/sc_softpull) that doesn't hurt your score but gives the lender the confidence they need to provide unsecured capital. This is the ultimate "win-win" for the time-crunched entrepreneur.

Protecting Your Personal Credit by Building Business Credit

One of the biggest mistakes we see business owners make, and we’ve seen a lot of them in our 23 years, is tying their personal identity to their business debt. If your business needs a $100,000 infusion to buy inventory or upgrade equipment, why should that appear on your personal credit report and lower your score for a future home mortgage?

Step-by-Step: How to Separate the Two

- Understand Personal Guarantees (Don’t Panic). Facilitating programs that focus on business performance allows you to keep your personal assets out of the line of fire. We are not telling you to stop offering a Personal Guaranty; rather, we want to clarify that having one does not necessarily mean your personal credit will be affected. A Personal Guaranty simply ensures that if a payment is missed, the principal can be contacted to cover it—a standard step for closely held companies. "Corporate Only" options (no personal guaranty) are typically reserved for companies with multiple shareholders not involved in daily operations, such as publicly traded firms.

- Incorporate and Get an EIN. If you haven't done this yet, do it today. It’s the first step to being "Simplified."

- Open Business-Specific Accounts. Never, and we mean never, mix your grocery money with your payroll funds.

- Use Business-Only Funding. Seeking unsecured working capital that reports to business bureaus (like Dun & Bradstreet) instead of personal ones is the "secret sauce" of the successful 2026 mogul.

By focusing on business-specific funding, you’re not just getting the capital you need; you’re building a "credit fortress" that protects your family’s financial future.

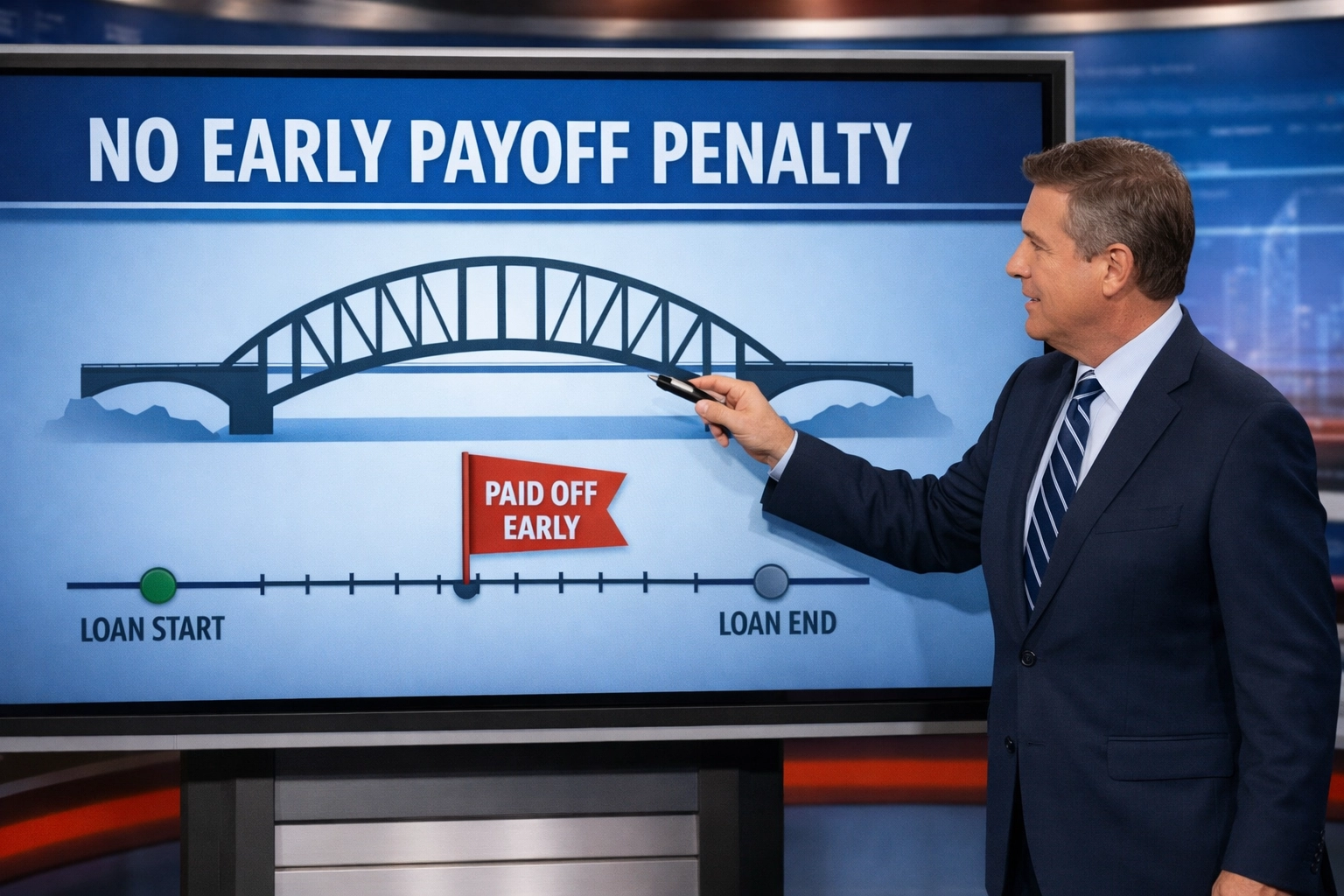

The "No Early Payoff Penalty" Revolution

If you’re an A or B credit business owner, you’re usually not looking for “money at any cost.” You’re looking for smart flexibility—capital you can use, control, and shut off the second you don’t need it anymore (because paying extra interest for fun is not a hobby).

That’s where our Working Capital Loans shine: these programs are built so you can pay off whenever you want, with no early payoff penalties. The cost of capital is simply a monthly rate, so the math stays clean and predictable.

- Flexibility (Use it when you need it). Access the funds, deploy them fast, and don’t get locked into paying for time you didn’t use.

- Control (Pay it off on your schedule). When that big receivable hits, the job wraps early, or your busy season ends, you can pay it down or off—your call.

- Savings (Only pay for the months you actually used). Example: if the annual cost is 24%, that’s 2% per month. Use the funds for 3 months and then pay it off? Your total cost of capital is 6% (2% x 3). Simple.

- Why it works (No “gotcha” penalty). This flexibility is made possible by an origination fee on each loan, which helps enable early payoff without penalties—so you’re not paying a surprise toll just for being efficient.

Think of it like turning financing into a dimmer switch, not an on/off trap: you use what you need, for as long as you need, then you move on—lighter, faster, and with more cash staying in your business.

Facilitating Programs: The Simplified Difference

You might hear a lot of jargon in the financing world, Working Capital Loan, MCAs, Term Loans, Lines of Credit, Equipment Financing. At the end of the day, you don't need a dictionary; you need a partner.

Since 2002, Simplified Capital has been the "calm in the storm." We don't just "sell loans"; we facilitate programs tailored to your specific industry and need(s). Whether you are in construction looking for materials financing or an auto shop owner servicing high-end EVs, the approach is the same:

- Speed: We know that in 2026, an opportunity today can be gone by tomorrow.

- Simplicity: Our application process is designed to be completed in minutes, not days.

- Support: You’re speaking to experts (Yup, you can actually speak to a knowledgeable adviser) who understand that a business is more than a balance sheet.

Practical Advice for the 2026 Entrepreneur

So, if you’re looking at your bank account and wondering if now is the time to grow, here is your "News Flash" checklist:

- Review your last 3 months of bank statements. Is the revenue consistent? If yes, you’re already 80% of the way to an approval.

- Check for "Non-Sufficient Funds" (NSFs). Lenders in 2026 hate to see bounced checks more than they hate a 620 credit score. Keep those balances positive!

- Identify your ROI. Don’t just take capital because it’s there. Use it for something that generates more money, new staff, better equipment, or bulk inventory.

- Protect your personal credit. Use the business’s strength to carry the business’s weight.

Conclusion: The Future is Funded by Cash Flow

Does your credit score matter in 2026? Yes, but it’s no longer the lead singer of the band: it’s the backup guitarist. The "Lead Singer" is your business’s cash flow and its ability to generate consistent revenue.

Don't let the fear of a credit score hold your ambitions hostage. Whether you're starting a new venture or scaling a legacy brand, there are facilitating programs designed to meet you exactly where you are.

Simplified Capital has been navigating these waters for 23 years. We’ve seen the trends come and go, but the one constant is that healthy businesses deserve fast, accessible, and fair capital.

Ready to see what your cash flow can do for you?

Stop guessing and start growing. Let’s look at your business's potential without the baggage of the past.

Apply Now or Contact Us to speak with a specialist today. Let’s make 2026 the year your business finally outpaces your expectations.

For more tips on managing your business growth, check out our blog or learn more about our mission.

Since 2002 (23 years), Simplified Capital—A+ BBB accredited—has helped small businesses secure fast, flexible funding. Need equipment financing, working capital, SBA/USDA options, construction materials financing, or business credit cards with intro rates as low as 0%? Call, email, or visit now for a free, no-pressure funding plan. Let’s make your next season of growth happen—together.

Website: www.simplifiedcapital.com

Phone: (866) 810-1305

Email: info@simplifiedcapital.com